European prices keep their uptrend

European gas prices rebounded on Friday, supported by technical buying after the strong drop of the previous session as the uptrend (fueled by low stock…

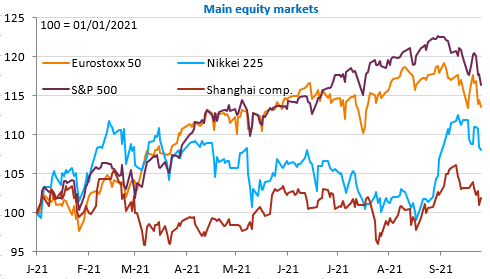

While September ended with the biggest decline in the US equity market since March, October starts with a sharp fall in Asia, particularly in Japan, despite a rather good BoJ (Tankan) survey. There is no shortage of cause for concern, as we have detailed here. To sum up, we have gone from “reflation trade” to “stagflation risk”, with aggravating factors such as the fall of the Evergrande property developer in China and the budgetary uncertainty in the United States, where everything fits together (infrastructure stimulus plan, deep economic reforms and debt ceiling), but nothing is materialising, except for a respite of a few weeks to avoid a new shutdown.

The fact that the Chinese authorities ordered the major energy groups to secure their supplies “at all costs” underlined the seriousness of the current crisis rather than reassured. Growing inflationary pressures should be further underlined by a further sharp rise in eurozone inflation (probably above the 3.3% consensus) today. The manufacturing PMIs are not expected to bring any surprises, but the price components in the US ISM survey will be watched closely. The August household consumption and income figures are also worth watching to fine-tune Q3 US GDP growth forecasts which are constantly being revised downwards.

The EUR/USD is settling below 1.16. Rising inflation in the eurozone doesn’t seem to be doing anything, but it could, if the numbers are really strong.