On second thought…

The markets, which had welcomed the Fed’s 75bp rate hike, finally revised their judgement significantly afterwards. Concerns about growth took over, leading to a sharp drop in…

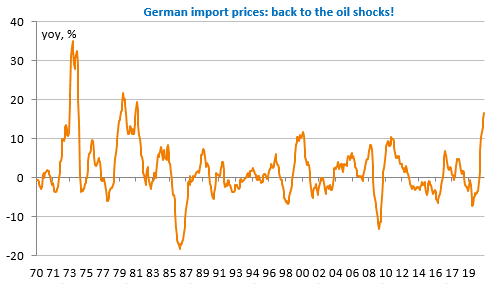

The US 10-year yield settled above 1.5%, up nearly 25bp over the week. The equity markets finally reacted, with tech stocks suffering the biggest losses (-2.83% for the Nasdaq). Inflationary pressures are not about to end, as evidenced by the surge in German import prices in August: +16.5% yoy, the first time this has happened since the 2nd oil shock.

Inflationary fears and the resulting changes in monetary policy are accompanied by bad signals on growth, particularly in China and the United States, and by one-off events or risks that create a toxic environment for the financial markets. The mechanics of this return of risk aversion are outlined here.

The decline in US household confidence and in particular expectations to their lowest level since the election of Joe Biden and the discovery of the Covid vaccines set off the fire yesterday. There are still a number of hurdles to clear this week before calm returns: Chinese PMIs tomorrow, Eurozone inflation and US household spending on Friday in particular, not to mention the debates over raising the debt ceiling and the Biden Administration’s stimulus plans.

The calendar is lighter today, awaiting the European Commission’s survey, the results of which could be quite good. Former Foreign Minister Fumio Kishida has just been elected to lead the LDP and is expected to become Japan’s Prime Minister on Monday. The euro continues to weaken against the US dollar as the ECB appears to be retreating from the monetary tightening process. The pound is also undergoing a clear downward correction due to the difficulties of the British economy: it is at its lowest since January against the greenback (1.35).