The reflation trade takes a break

At least the movements on the financial markets were consistent yesterday. Equity markets were down and even sharply down in Europe. In parallel, after an…

Long-term interest rates fell again, although they are a bit on the rise this morning: the US 10-year is trading at 1.53%. US producer prices recorded their smallest increase of the year for the month, although they continued to accelerate yoy. This does not call into question the expected tightening of US monetary policy in early November as the key issue is employment, and jobless claims fell below 300k for the first time since the pandemic began. The dollar is falling (EUR/USD > 1.16) in a context where investors are returning to equities, thanks to very good corporate results (and lower long-term rates).

The plunge in European car registrations in September (-23.1%) confirms the impact of the semiconductor shortage on supply, while potential demand is strong.

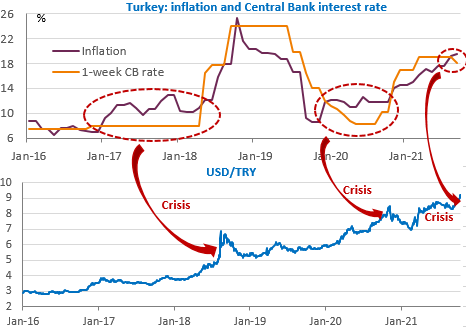

The Turkish lira continues to plummet: it has lost 25% of its value against the USD since the former Governor of the Central Bank was dismissed in February. Three new central bankers suffered the same fate on Wednesday evening. We can therefore assume that further rate cuts are coming, while the inflation rate approaches 20%.

Today’s main focus is on US retail sales in September as well as the University of Michigan consumer survey, import prices and the New York Fed survey. A serious test for the bond market.