Gas & Power Report: Energy prices remain under bearish pressure in Europe

Gas & Power Podcast #45 In this week’s Gas & Power podcast, Julien Hoarau discusses about the reduction of the contango on the EU as…

Spectacular decline in bond yields: the US 10-year ended the week at 2.88%. It was at 3.47% in mid-June. The German Bund fell from 1.76% to 1.22% in 10 days. The markets are totally focused on the effects of monetary policy tightening and signs of economic slowdown. The dollar continues to be very strong: the EUR/USD exchange rate touched 1.0366 before rebounding above 1.04. The decline in the manufacturing ISM index from 56.1 to 53 in June reinforced the feeling that the US economy had already decelerated. The Atlanta Fed is even forecasting a contraction in GDP for the second consecutive quarter in Q2, the definition of a recession. We had identified this risk in this note published on June 17. In parallel, the lack of room for manoeuvre for central banks at this stage was again illustrated on Friday by the rise in the eurozone inflation rate from 8.1% to 8.6% in June, despite a temporary dip in the inflation rate in Germany.

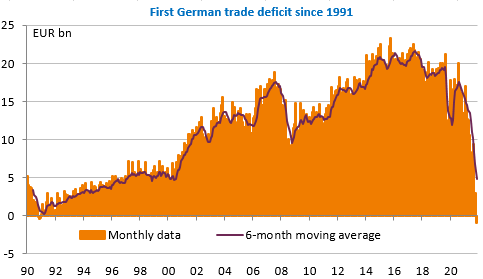

Independence Day in the US. Few economic indicators to move the markets as a result. German foreign trade data in May did show the first deficit since 1991 with a decline in exports. The war in Ukraine and the Covid in China are having devastating effects on German industry.

Eurozone producer prices are also expected, still up over 35% year-on-year. But news from China, where Covid cases are again on the rise in the east of the country, around Shanghai, is likely to dominate attention after Xi Jinping reaffirmed the wisdom of the country’s zero Covid strategy.