EUAs posted 4.2% gain on strong auction result

The power spot prices rebounded yesterday in Germany, Belgium and the Netherlands amid forecasts of easing renewable generation, but slightly fade din France on expectations…

The equity markets have been on the decline for the past two days. Confidence in a quick peace in Ukraine has frankly and logically declined. The vagueness surrounding the payment of Russian gas sales to European countries also raises the threat of an interruption of flows, even if no one really envisages that this scenario will materialise.

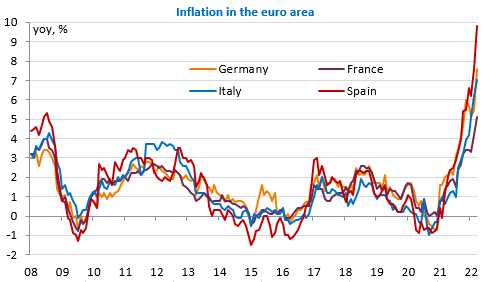

With all Euro area countries posting slippages, inflation in the region is expected to reach or exceed 7% in March.

Bloomberg economists now estimate that energy bills will rise by €230bn for eurozone consumers. In February, their estimate was €100bn! Downward revisions to the growth outlook are increasing. Bloomberg has cut its forecast for eurozone growth from 4.3% to 2.6% this year (our forecast is 2.2%). The German economic institutes have done the same for Germany even more dramatically: +1.8% versus +4.6%. For different reasons (pandemic), forecasts for China have also been revised downwards: Morgan Stanley has just lowered its forecast from 5.1% to 4.6%. The Caixin industrial PMI fell more than expected in March, from 50.4 to 48.1. This morning, the Tankan survey in Japan showed a clear deterioration in the outlook. In contrast, the PMI did not decline in Japan. With the exception of China, the first PMI estimates remained surprisingly good, especially in the eurozone. We will see if this is confirmed today with the release of the final indices as the other surveys all showed a marked deterioration.

Apart from the Eurozone inflation figures and the industrial PMIs, we are waiting for the US job report with the evolution of wages to watch, as they had unexpectedly slowed down last month. The ISM manufacturing index is also worth watching. The EUR/USD exchange rate is falling towards 1.1050, a sign that market confidence is waning.