Markets unnerved by tensions with Russia

Equity markets fell sharply yesterday, particularly in the US, after a US official warned of an “imminent invasion” of Ukraine by Russia. The flight of investors…

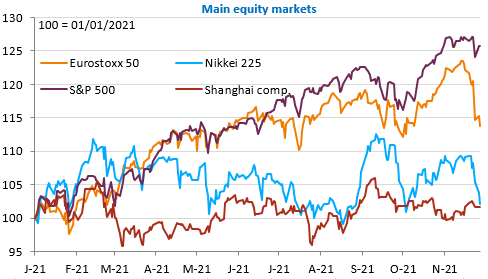

I’ll start with the bad one as it explains the relapse of risky assets after yesterday’s rebound: Brent crude oil price close to $70/b, US 10-year yield below 1.45%, equity markets down in Asia and Europe this morning. The EUR/USD exchange rate is up to 1.134.

Moderna’s CEO gave an interview to the FT in which he gave 3 messages: 1. there is a very high probability that existing vaccines will be largely ineffective against Omicron due to its multiple mutations, 2. a new vaccine is conceivable for early 2022, but 3. Its production and distribution will take months.

The good news now is that initial feedback from South African doctors is that infected people have mild symptoms, not at all comparable to the Delta variant. Of course, all this needs to be confirmed, but if this second piece of news is confirmed, we would see another sharp turnaround in the markets as it would greatly reduce the risks to economic activity.

In terms of economic indicators, China’s manufacturing PMI rose back above 50, confirming the easing of coal shortage tensions (after the rebound in production). Eurozone inflation figures for November are awaited, which could exceed expectations (consensus 4.5% yoy), given the slippage in Germany (+6%). This should not call into question the ECB’s caution. Even the Fed could finally delay announcing an acceleration of its asset purchases. This is suggested by the speech full of uncertainty that Jerome Powell is due to deliver before the Senate today. Also worth watching is the Conference Board’s consumer confidence index.