Chinese runs in March remained strong

ICE Brent prompt month reached 67.1 $/b on early Thursday, as the dollar continued to weaken and new data on the Chinese refining sector showed sustained…

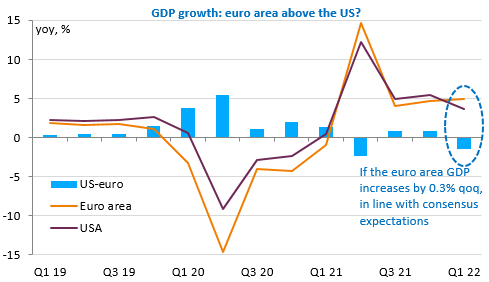

Surprising contraction of the US GDP in Q1 (-1.4% qoq annualised): as expected, inventories contributed negatively to growth, as did public spending, but it was above all foreign trade that weighed on growth, with a very sharp rise in imports (+17.7%) and a decline in exports (-5.9%). But the core of growth, private domestic demand (consumption, productive and residential investment), is showing solid growth, which explains why these figures have been received calmly. The Fed is in a bit of an awkward position, but should nevertheless raise its key rate by 50bp next week.

The euro area is next with Q1 GDP growth and April inflation: GDP is expected to rise by 0.3% despite the impact of Covid at the beginning of the period and the war in Ukraine at the end. Germany should have escaped recession but Italian GDP is expected to fall and the stagnation of French GDP (with a 1.3% fall in household consumption) is the bad surprise of the morning. This forecast for the Eurozone now looks optimistic. As for inflation, it again exceeded expectations and rose to 7.8% in Germany and 5.4% in France, but fell sharply in Spain. For the eurozone as a whole, it is expected to remain stable at 7.5%.

The markets are well oriented, reassured by the US corporate results and still hopeful of measures to support activity in China. The euro is recovering slightly against the USD around 1.0550 after touching 1.0472 yesterday.