Inflation fears

It’s paradoxical but the poor US jobs report has brought inflationary fears back to the forefront of market concerns. The Nasdaq plunged by 2.6% yesterday…

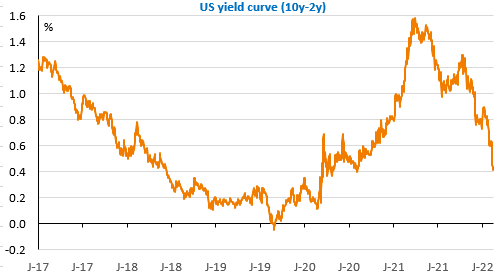

The markets are on tenterhooks, watching for the slightest signal that tensions with Russia are easing or that an invasion of Ukraine is imminent. Equity markets fell sharply in Europe yesterday. Volatility was high in the US, but losses were limited. The US 10-year yield rose above 2% before falling back below it again. The dollar strengthened to 1.128 against the euro, but is now back above 1.13. Risk aversion remains dominant but volatility is high. Concerns about inflation and monetary policy remain as strong as ever. Markets are now anticipating up to seven 25bp rate hikes before the end of the year. The flattening of the curve clearly signals a growing concern about growth.

Japanese GDP rose strongly in Q4 2021 (+1.3%), between the Delta and Omicron waves. Further acceleration in UK wages in December, which only reinforces rate hike expectations.

We are waiting for the ZEW survey this morning and revised GDP figures for the euro zone in Q4 2021, but above all, producer prices and the New York Fed survey in the US. The main driver will nevertheless remain the evolution of the situation in Eastern Europe.