EUAs fell alongside the fuels and oil markets

The power spot prices slightly faded in northwestern Europe yesterday amid forecasts of weaker demand, stronger solar generation and higher French nuclear availability, although the…

The equity markets rebounded sharply, Treasuries (rates up) and the dollar (EUR/USD > 1.1350) fell, and of course energy prices rose. The announcement that some of the Russian troops that were massed near the Ukrainian border have returned to their garrison has both significantly reduced risk aversion and put inflation back in the spotlight.

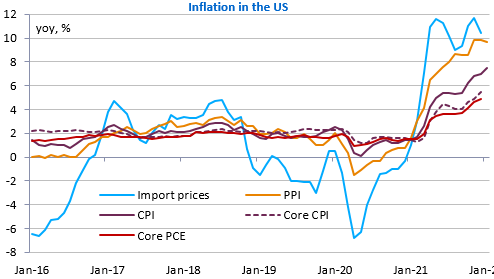

This is all the more true as US producer price figures surprised on the upside again in January: admittedly, their rise has levelled off (+9.7% after +9.8% yoy), but they rose twice as fast as expected mom (+1%). The 10-year rate has risen above 2%.

This morning, the inflation rate also exceeded expectations in the UK: +5.5% yoy in January. The exception is China, where inflation is down to 0.9% yoy, mainly due to a sharp decline in pork prices. This paves the way for monetary easing by the PBoC, which is also totally at odds with what is happening in the West.

If the détente between Russia and NATO is confirmed, the rate hike could be reinforced with the publication today of US industrial production figures in January and, above all, the Minutes of the last Fed meeting which could highlight the desire of part of the Board to accelerate monetary tightening.