A dead cat bounce?

US equity markets bounced back on Tuesday, reversing some of the sharp losses recorded last week on the back of an historical 75 bp interest…

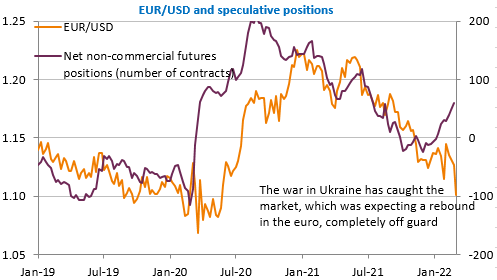

Unsurprisingly, the markets fell back into pessimism yesterday, with stocks recording substantial declines, again particularly in Europe (-2% for the Eurostoxx 50, bringing its decline to 13% since the beginning of the year, compared with -0.5% and -9% respectively for the S&P 500 in the US). The rebound that accompanied the Fed chairman’s speech on Wednesday was therefore nothing more than a flash in the pan. Long-term interest rates also fell (the US 10-year fell back below 1.8%) and the USD strengthened to almost 1.10 against the euro, a level not seen since spring 2020. The risks are on the downside as the market is totally caught off guard as shown in this chart.

There is too much uncertainty about the outcome and consequences of the Russian invasion of Ukraine for confidence to return so quickly, and the events of last night will not change this as a missile hit Europe’s largest nuclear power plant in Zaporizhzhia in south-eastern Ukraine, fortunately without dramatic consequences according to the latest information.

In addition to the problem of energy supply in Europe, several sectors are beginning to report the suspension of factory activity due to shortages of intermediate goods manufactured in Ukraine or of raw materials. This is the case of the automotive sector in Germany (wiring harnesses) or the steel industry in Italy (pig iron). The problems of disruption in the production chain caused by the pandemic will become more acute, contributing both to inflationary pressures and to the restriction of activity.

Today the US job report will be released. Given the huge surprise of the January numbers (upwards), anything is possible and the risks are asymmetrical: a high number would not change expectations about the Fed, which is forced to arbitrate between inflationary risk and the threat to growth from the war in Ukraine. But a disappointing result could lead the markets to significantly revise downwards their expectations of monetary tightening.