Fears of a return in inflation will accompany the recovery

The rally in US stocks was interrupted yesterday, mainly on inflation fears that have been strengthening significantly since Joe Biden unveiled his $1.9tn stimulus plan.…

Stagflationary risks continued to cloud the European economic horizon on Tuesday with growing concerns over the impact of a potential ECB monetary policy tightening on the EU GDP growth. The ZEW index, which measures investor expectations for the German economy, plunged from 54.3 in February to minus 39.3 in March, close to the all-time low of minus 49.5 reached in March 2020 at the beginning of the Covid crisis. In Asia, Chinese tech stocks posted a strong rebound today after a selloff on concerns over a resurgence in Covid-19 cases and the impact of potential sanctions linked to a possible support to Russia in its war against Ukraine.

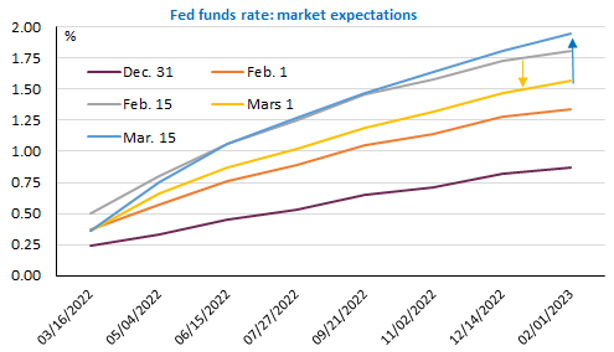

The main event on the agenda today is of course the Federal Open Market Committee. And with the first Fed rate hike looming this evening, market expectations have returned to where they were before the outbreak of war in Ukraine, putting growth risks completely aside to focus on inflationary risk, exacerbated by soaring commodity prices. The markets are anticipating nearly seven 25bp hikes between now and the end of the year, with a high probability of a 50bp hike in May or June.

The update of the Fed’s economic forecasts and the rate forecasts of its members (the “Dots”) will be crucial to determine whether the markets have gone too far or whether the Fed is determined to tighten its policy “whatever It takes”.