Financial markets remain focused on the US stimulus package

Equity markets were down on Friday after the release of indicators pointing to recession in Europe, concerns heightened by the announced delays in vaccine deliver.…

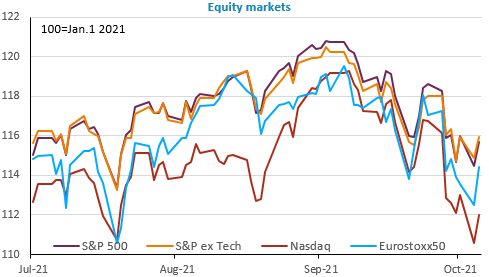

Yesterday’s sharp rebound in equity markets should quickly come up against the wall of interest rates: the US 10-year yield rose above 1.57% this morning, its highest level since June. Inflation expectations are simmering. The 10-year break-even inflation rate in the UK is above 4% for the first time since 2008. Asian markets have already turned around and European markets open lower. The dollar is logically strengthening in such a context: the EUR/USD exchange rate is approaching its lowest level of the year (1.1563).

The services PMIs released yesterday confirmed the solid pace of growth in Europe and the US, now that the threat of the Delta variant is receding. The ISM index even surprised positively in the US at 61.9, with the price index rising again. German factory orders, on the other hand, fell sharply in August (-7.7% m/m), but this was mainly due to bottlenecks in certain sectors, starting with the automotive sector (-12% m/m), which reinforces inflationary concerns.

Today, euro area retail sales are expected to rise in August and we will also be watching ADP’s September private employment estimates in the US, ahead of Friday’s employment report.