Physical trade boost

Crude prices climbed back above 74 $/b at the prompt, confirming that the liquidation experienced last week could be short-lived. Indeed, geopolitical risk in Saudi…

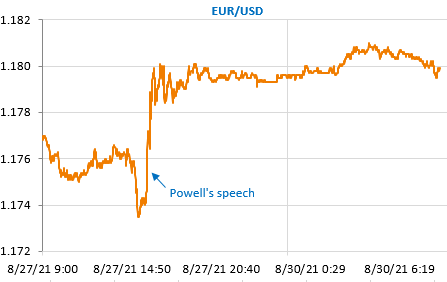

The markets welcomed the Fed Chairman’s speech at the Jackson Hole symposium. He confirmed the strong likelihood that the Fed will begin to reduce its asset purchases before the end of the year, but gave no specific information on the timing and pace of this operation. The markets especially appreciated the fact that he disconnected a possible increase in key rates from this reduction in asset purchases.

Please refer to our commentary on Jerome Powell’s speech published on Friday and to the latest Weekly Economic Outlook on the key issue of inflationary risk in the US.

Equity markets continued their positive trend in Asia. Long term bond yields are slightly lower (US 10 year is back below 1.3%) and the dollar is not gaining any ground for the moment after Friday’s drop (EUR/USD at 1.18).

The European Commission’s survey and the first inflation figures for August in the Eurozone should be watched today, with a further acceleration expected in Germany to 3.4%, which could continue to support the euro against the USD.