Mrs. Yellen reinforces stimulus bets and boosts risk appetite on financial markets

Mrs. Yellen could be confirmed as Treasury Secretary as soon as tomorrow, after Mr. Biden officially becomes President of the US today. Her hearing at…

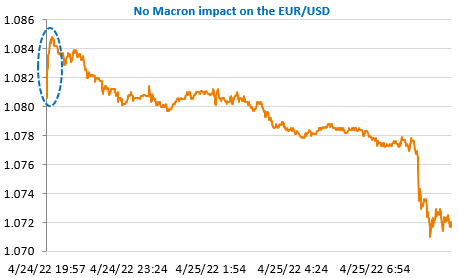

There is no sign of euphoria either in the population or on the markets after the re-election of Emmanuel Macron in France: the bond yield spread against Germany is stable and the very brief surge of the euro has given way to a plunge to a new 2-year low against the USD, just above 1.07. His victory over Marine Le Pen is nevertheless larger than expected (58.5% vs 41.5%), but the high abstention rate presages great political uncertainty before the legislative elections of 12 and 19 June.

The dominant trend on the markets is dictated by expectations of very strong monetary tightening by the Fed in particular and the worrying news from China where the pandemic is now spreading to Beijing, leading to the same restrictive measures as those that affected Shanghai. After falling sharply on Friday (-2.8% for the S&P 500 and -2.2% for the Eurostoxx 50), the equity markets remain on the same trend with strong declines in Asia.

And of course, there is no sign of improvement in Ukraine where negotiations seem to have been abandoned. The PMI surveys published on Friday sent surprisingly reassuring signals about the business climate in Europe, including in industry, which is known to be facing major shortages. The manufacturing PMI held up at 55.3 and the services PMI rebounded to 57.7. The publication of the April German IFO survey this morning (it was much more alarmist in March) will allow us to confirm or refute the PMI results. A further deterioration could accentuate the decline in the euro.