Macro & Oil Report : Lower interest rates for better or worse?

Macro & Oil Report: Lower interest rates for better or worse? Macro & Oil #121 Rates fall sharply in the US, but caution in the…

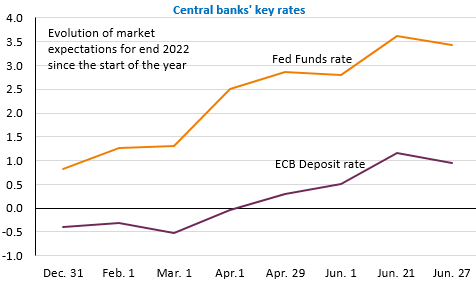

The rebound in risky assets that began on Thursday after the publication of sharply lower PMIs was amplified on Friday after the revised figures from the University of Michigan’s consumer survey showed a drop in inflation expectations. The S&P 500 was up 3.1% and the Euro Stoxx 50 2.8%. The EUR/USD exchange rate is up, above 1.0570. It was this rise in inflation expectations that led the Fed to hike its key rate by 75bp at its last meeting. The observation is therefore clear: risky assets are rebounding because the markets are revising downwards their expectations of monetary tightening. They no longer expect a 75bp increase in the Fed funds rate in July and see the rate hike ending in December. But this rebound appears very fragile as it also means that the risks of recession are on the rise.

Chinese manufacturing profits contracted by 6.5% year-on-year in May. This is slightly less than in April (-8.5% yoy) thanks to the timid recovery of activity with the gradual lifting of anti-Covid measures.

Russia has defaulted on its foreign currency debt: $100 million of interest payments due on 27 May have not been settled. The grace period has therefore expired. This is the first time this has happened since the Bolshevik revolution of 1917 and the non-recognition of the Tsar’s debt.

To be watch from today the meeting of the central bankers in Sintra, near Lisbon. Given the main reason for the market rebound, what is said there will be closely scrutinised!