Another day of muted activity in the power and carbon markets

The NWE power spot prices slightly rebounded yesterday, buoyed by forecasts of lower renewable generation, while an improving nuclear availability kept the French prices steady…

The US 10 year yield rebounded by 15bp yesterday to 1.87%, as oil prices soared and the Fed Chairman spoke to members of the House of Representatives. The Fed Chairman confirmed that the Fed would indeed raise its key rate by 25bp at its next meeting and of course stressed the fact that the war in Ukraine had introduced a great deal of uncertainty for the conduct of monetary policy. He said that the Fed would not hesitate to accelerate monetary tightening to fight inflation while taking into account the possible negative impact of the war on the US economy. Equity markets seemed reassured by the speech, rising between 1.5% and 2% but it is hard to understand why. The risks that they will fall again quickly, especially if the Russian army confirms its advance on Ukrainian soil and oil prices continue to rise, seem very high. The EUR/USD exchange rate does not move much around 1.11.

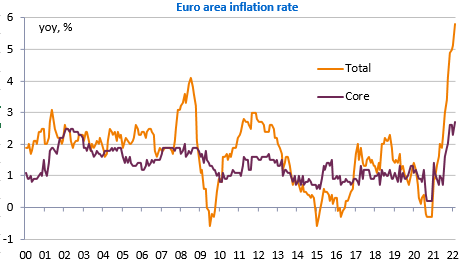

Central banks are in a very delicate situation: the dominant tone of Jerome Powell’s speech was that the US economy should be able to withstand the monetary tightening necessary to curb inflation. As far as the ECB is concerned, it is more complicated: inflation accelerated again in February to 5.8% and the European economies are much more exposed to war in Ukraine than the US economy.

There may be some interesting elements in the discussions of the last ECB meeting which are published today, but the possibility of a Russian invasion of Ukraine still seemed remote at the time. The main economic data of the day are the services PMIs and the jobless claims in the US. Jerome Powell is speaking in front of the Senate this time, but it is hard to see what else he could say compared to yesterday.