Prices maintain their bullish trend

European gas prices were up overall yesterday, still supported by uncertainties on Russian supply and LNG flows (following the shutdown of the US Freeport LNG…

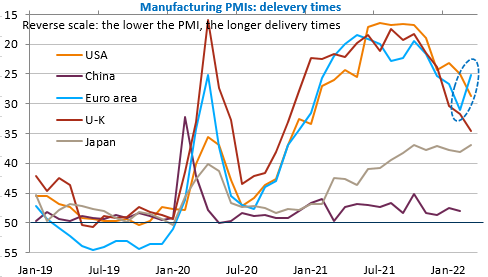

March PMIs generally came out better than expected, particularly in the US where they were up sharply in both manufacturing and services. This probably helped (in addition to a specific rebound in technology stocks) to support a further rise in US equity markets as well as the decline in weekly jobless claims to their lowest level since 1969. Long-term rates stabilised at high levels and the EUR/USD exchange rate rose very slightly above 1.10. The markets are awaiting announcements that may be made to close the US President’s visit to Europe but it seems that this will mainly concern US LNG sales to Europe to reduce imports from Russia.

The Eurozone PMIs nevertheless showed a sharp rebound in delivery times and additional pressure on both input and output prices. Rising inflationary pressures explain why markets continue to expect almost two 25bp rate hikes from the ECB by the end of the year, even though the probability of a sharp economic slowdown is quite high.

It will be interesting to see this morning if the IFO survey in Germany reflects a more pronounced concern from manufacturers than the PMI survey, as was the case with the INSEE survey for France yesterday. We will also have the ISTAT survey in Italy and the pending home sales in the United States where the strong rise in long-term rates is starting to worry real estate professionals.