Strong price rebound

European gas prices continued their rebound yesterday, posting strong gains as they got support from the rise in Asia JKM prices (+7.15%, to €82.262/MWh, on…

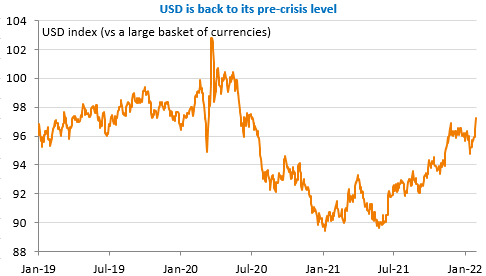

The markets are very volatile after Jerome Powell’s statements. They are now expecting almost five 25bp hikes in the fed funds rate by the end of the year (for seven meetings). Should we be worried about the risk of inflation or should we be happy that the Fed is finally taking the problem head on? Will growth hold up? These are the questions that are driving the constant back and forth in equity markets (down in the US yesterday) and interest rates. There is an additional source of volatility with the news from the Chinese real estate sector where there is a wave of resignations of the auditors responsible for certifying the accounts of the sector. The only constant is the clear strengthening of the dollar (EUR/USD @ 1.1150!).

Economic news: robust activity in Q4 2021 in the US, where GDP grew by 6.9% in annualised quarterly variation. Same thing in France where growth exceeded expectations: +0.7% qoq. Only in Germany is a contraction expected, due to the Delta variant. The figures will be known this morning. Many other economic reports are expected: Spanish GDP, European Commission survey and US household spending in December with above all the evolution of the core PCE deflator, the inflation indicator favoured by the Fed. The markets should remain agitated.