Rising bond yields still do not shake market confidence

Who could have predicted such a phenomenon? Bond yields continue to rise sharply: the US 10-year has reached 2.4%. The 2-year rate is already at 2.2%,…

Fed members are making more and more statements in favour of a strong and accelerated tightening of monetary policy. The market is pricing in 87% for a 50bp increase in the Fed funds rate in May. At that time, the Fed could also announce the pace at which it will reduce the size of its balance sheet, which should increase the negative pressure on the bond market (i.e. push up yields). The US 10-year yield is capped at around 1.3-1.4% for the time being, as markets alternate between confidence and concern about growth. Yesterday, equity markets logically (we explained why yesterday morning) retreated, but it is clear that at this stage, the prevailing sentiment remains that the US economy is capable of absorbing the double whammy of the consequences of the war in Ukraine and the monetary tightening.

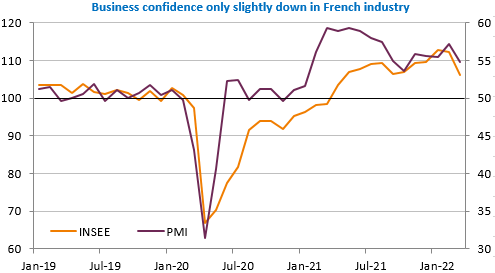

The March PMIs have started to be published as well as the INSEE survey in France. The latter shows a clear downturn in the business climate, particularly in industry. But it remains above its long-term average. The rise in uncertainty and the prospects of price rises and a slowdown in production (linked to supply problems) stand out in particular. The most affected sectors are automotive and chemicals, not food at this stage.

Japanese PMIs have risen while the result is mixed in France: rise in services but decline in industry, confirming Europe’s overexposure to the war in Ukraine. Jobless claims, durable goods orders and PMIs will be published in the US. The EUR/USD exchange rate fell back below 1.10 but did not show any significant variation.