Awaiting key US indicators

The US bond market was closed yesterday, bringing some calm after a sharp rise in yields last week that was not halted by the release…

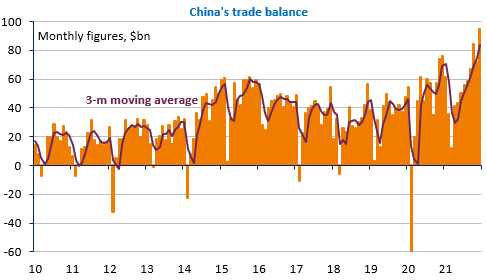

China has achieved a record trade surplus of $676 billion in 2021, thanks to the strong recovery in global demand for materials (steel), consumer goods and products specifically related to the pandemic (para-medical equipment). The relative weakness of domestic consumption has at the same time limited imports. This trend should be confirmed in 2022: China will be anything but a locomotive for the world economy, with a much lower growth rate (around 5% compared with over 8% in 2021) and a strong contribution from foreign trade.

But this is not yet the main concern of the markets, which are once again worried about the Fed’s stated intention to increase monetary tightening as soon as the Omicron wave ends: the Nasdaq fell heavily (-2.5%), dragging down the USD, which hit 1.1483 against the euro. The growing tensions between Russia and NATO are another source of concern, especially as they could contribute to the rise in inflation via energy prices.

The day’s economic agenda is extremely busy. Activity in the UK was much stronger than expected in November (GDP grew by 0.9% mom) ahead of the Omicron wave. The first estimate of German GDP growth in 2021 will be published this morning before a number of US indicators this afternoon: retail sales and industrial production in December, consumer confidence in January. We can expect quite high volatility today.