The soaring gas prices continued to push EUAs to fresh records

The power spot prices edged down yesterday in north western Europe, torn between forecasts of stronger wind output but weaker solar generation and slightly lower…

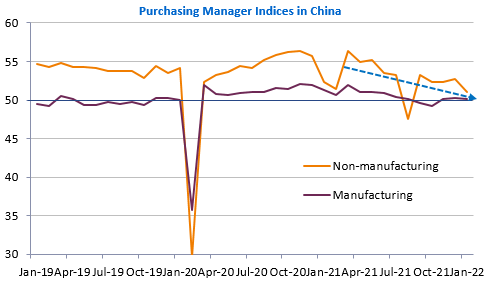

The US equity markets ended the week with a bang, with the Nasdaq up 3.1%. Long-term rates are slowly rising (10-year US at 1.79%) and the USD is giving up some ground at 1.1170 against the euro. All this seems to confirm a decline in risk aversion. However, the Atlanta Fed President confirmed that a 50bp increase in the Fed funds rate was possible. The US is also preparing sanctions against Russia, even without an attack on Ukraine and finally, China’s PMIs published yesterday showed a clear slowdown in the economy: 50.1 in the manufacturing sector and even 49.1 for the Caixin index, 51.1 in the non-manufacturing sector (services and construction).

Today, GDP growth in the Eurozone in Q4 2021 is expected to be rather weak (+0.4%) due to the fall in activity in Germany (-0.7% qoq). We are also waiting for the German inflation rate in January, which is expected to fall sharply (4.3% yoy after 5.7% according to the consensus) due to the consumption tax increase in January 2021. These two figures will potentially have an impact on the ECB’s monetary policy expectations and could therefore move the EUR/USD exchange rate.