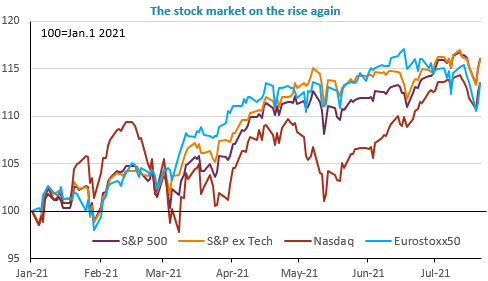

Concerns about the spread of the Delta variant seem to have significantly diminished suddenly: bond yields rebounded, the US 10y nearing 1.3%. Stock markets were on the rise, sharply in Europe with increases of around 2% on average, and commodity prices rebounded as well, led by oil. The USD weakened logically in this context and the EUR/USD exchange rate edged up to 1.18, while the GBP rebounded (EUR/GBP now trading below 0.86).

Nothing particular to explain this change of trend except the fact that pessimism was likely excessive and, above all, the fall in bond yields difficult to justify. This being said, it looks like these erratic market moves could continue, as no good news on the spread of the delta variant can be expected in the foreseeable future.

On the agenda today, the ECB meeting with changes expected in its guidance to reflect its strategic moves, but we doubt it can really surprise markets. US jobless claims and the leading index in the US as well as the CBI survey in the UK.

Negotiations resume in Turkey between Ukrainian and Russian representatives with a view to reaching a ceasefire. The Ukrainian counter-offensive on the ground suggests that the balance…

Concerns about the spread of the Delta variant seem to have significantly diminished suddenly: bond yields rebounded, the US 10y nearing 1.3%. Stock markets were on the rise, sharply in Europe with increases of around 2% on average, and commodity prices rebounded as well, led by oil. The USD weakened logically in this context and the EUR/USD exchange rate edged up to 1.18, while the GBP rebounded (EUR/GBP now trading below 0.86).