European gas prices weakened again

European gas prices weakened again yesterday, still pressured by lower heating demand due to rising temperatures. The drop in parity prices with coal for power…

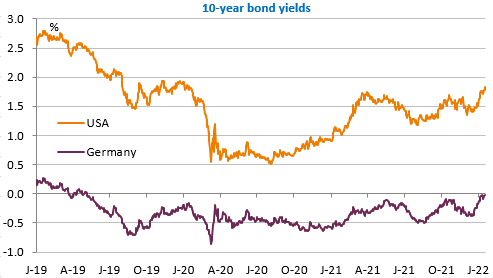

Soaring oil prices are (rightly) fuelling inflationary fears. Inflation forecasts have been revised upwards significantly, as shown by the latest survey conducted by Bloomberg: +0.3% compared to the December survey on the annual average for 2022 for US inflation (4.6% against 4.3% previously). The market is now anticipating four 25bp rate hikes by the Fed this year and bond yields are rising: the 2-year rate has just risen above 1% for the 1st time since February 2020. The 10-year rate is following the same trajectory (1.83% now). Although the ECB appears to be lagging far behind the Fed in its monetary policy normalisation process, rates are rising in the eurozone too: the German 10-year rate is about to touch 0% for the 1st time since spring 2019.

In Japan, the central bank now considers the inflation outlook to be “balanced” (not downward) for the 1st time since 2014. In the UK, labour market figures released this morning suggest that the BoE may raise its key rate again in February. Against this backdrop, it looks like a difficult day for risky assets, starting with the equity market. The USD rallied slightly to 1.14 against the euro.

The economic agenda of the day is provided without containing any really key indicator, just like what is going to happen this week: ZEW survey in Germany, New York Fed index in industry, NAHB survey in the construction sector and long capital flows in the United States.