Cushing-centric demand

ICE Brent crude oil remained at 68.9 $/b, as the API survey showed a continued drop in US crude stocks while refined product stocks dipped…

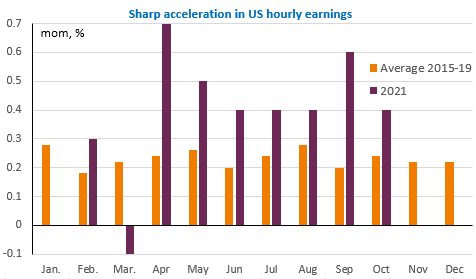

The easing in bond yields that began after the Fed meeting and especially the Bank of England’s decision to postpone monetary tightening continued on Friday after a very solid US employment report: job creation picked up and wages continued to accelerate (more details here).

The markets focused on the fact that the participation rate did not rise, concluding that the Fed would continue to be accommodative until the labour market normalized. But labour shortages are helping to drive wage increases. And the Fed’s comments were not particularly dovish on Wednesday. Friday’s vote on the $1200bn infrastructure spending plan by the US Congress is another element in favour of a tightening of monetary policy. Nevertheless, US and German 10 year yields fell by 15bps on Thursday and Friday and equity markets hit new record highs. The EUR/USD exchange rate stabilised above 1.155.

Chinese foreign trade figures were released yesterday and again showed solid growth in exports (+27.1% yoy) and imports (+20.6%) despite slowing domestic demand.