Core inflationary tensions are building in the US

The Fed’s preferred measure of inflation accelerated to +3.1% yoy in April, but equities advanced further and the 10y bond yield fell below 1.6%. Markets…

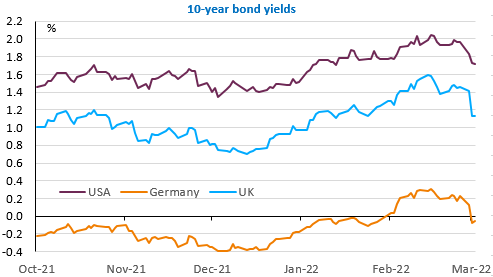

We were trying to find explanations for the wait-and-see attitude of the markets yesterday. It didn’t take long for this attitude to be shattered: energy prices literally soared as the fighting in Ukraine intensified. This led to a rally in the bond markets and the dollar and a plunge in the equity markets. This has been particularly the case in Europe where there are fears that the war in Ukraine will have a very negative impact on growth, so despite the likely increase in inflation, the markets are no longer expecting the ECB to raise rates this year. Long-term rates fell sharply, by 20 to 30 bp on 10-year maturities in the euro zone, with the German 10-year rate going negative again. And of course, equity markets fell sharply, by around 4%. Movements were less pronounced in the US, but the markets are now expecting only 4 rate hikes from the Fed this year and are no longer fully expecting a 25bp increase in the Fed funds rate in March. Despite this, the dollar is strengthening and has just broken the 1.11 support against the euro.

It is an understatement to say that the day promises to be rich in events that should further fuel high volatility on the markets: we expect a new rise in the inflation rate of the euro zone towards 5.5% in February. The ADP US private employment figures will also be published. Most importantly, OPEC meets to decide on its production quotas and Jerome Powell appears before the House of Representatives to report on his policy. Let’s not forget that in parallel, the Bank of Canada is expected to raise its key rate, which should underline how the consequences of the war should be less on the other side of the Atlantic.