TTF year-ahead prices breach the €22/MWh level

Prospects of below-average temperatures in the coming two weeks, a tight supply picture and soaring coal and EUA prices pushed European gas prices further high on Tuesday. The coal API…

The rebound in European equity markets could continue after Evergrande announced that it had reached an agreement with its creditors on the payment of interest tomorrow on a yuan loan. This seems to confirm that the Chinese authorities will “convince” the domestic creditors to rearrange the repayment terms to avoid a formal default by the property developer. However, there was no word on the interest payment (again on Thursday) on another USD loan ($83.5m), which means that this respite could be short-lived.

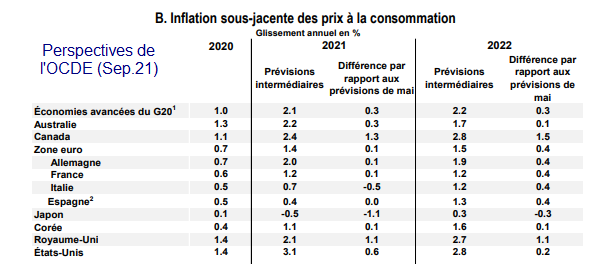

In addition, US markets just stabilised yesterday, already looking ahead to the Fed meeting that ends today. It seems almost a foregone conclusion that the Fed will postpone the announcement of the reduction of its securities purchases until the next meeting (early November). The main risk in our view is that Fed members’ rate forecasts show an increase in the probability of tightening as early as 2022 in the face of rising inflationary risk, further highlighted by yesterday’s sharp upward revision of the OECD forecasts.

The EUR/USD exchange rate seems to be stabilising around 1.1720-30.