Second attempt for the Parliament

The European power spot prices were mixed yesterday, lifted in Germany and France by the higher fuel and carbon prices but down in Belgium and…

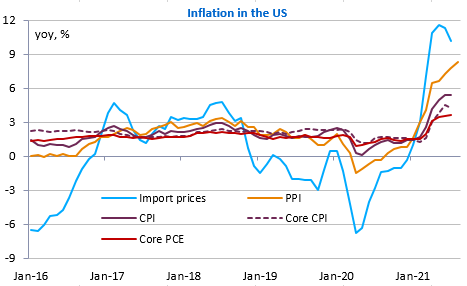

With one week to go before the next Fed meeting, the August inflation figures for the US are of particular importance. A very slight drop is expected, but the inflation rate could be above 5% for the 4th month in a row, while core inflation has been above 4% for the last two months. Energy prices remain very high and even rebound in September due to the hurricanes. On the other hand, producer prices accelerated to +8.3% in July due to multiple bottlenecks and recruitment difficulties affecting some sectors.

In this respect, it will probably be at least as interesting to look at the results of the NFIB survey (small businesses), which gives indications of their difficulties in hiring and their intentions in terms of wage and selling price increases. Bond yields are stable and the EUR/USD exchange rate is back to just above 1.18.