The risk of stagflation is more relevant than ever

The reaction of the markets to the Fed’s announcements yesterday says a lot about the extreme nature of their expectations: the Fed increased its Fed…

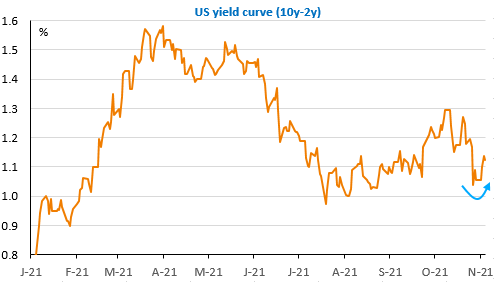

Unsurprisingly, the Fed announced yesterday the start of the reduction of its asset purchases. We already commented on this decision last night (here). Since then, it is confirmed that the markets have welcomed it, with the US main stock market indices reaching new records. The yield curve has steepened a bit (bond yields have risen more on long maturities), but this is mainly a correction of the recent flattening that reflected fears of a brutal monetary tightening that would break growth.

What we can retain from Jerome Powell’s press conference is a great humility regarding the inflation outlook. In reality, the Fed does not know whether the current slippage will not become entrenched. What it does know is that the factors driving inflation upwards, i.e. business supply problems and recruitment difficulties, are lasting longer than it thought and are not showing any signs of abating, as the ISM services survey showed yesterday. An unpleasant surprise for the markets would be an acceleration in the pace of asset purchases and a premature rate hike in the wake. For now, markets are expecting this in July 2022.

Today, it is the Bank of England that is in the spotlight: the markets are expecting a 15bp increase in the base rate before the end of the year, but there is some doubt about the timing between November and December. The pound has rallied since the beginning of the week, suggesting strong expectations for today. Markets are of course focused on the inflation outlook and in this regard will be watching closely in parallel to the OPEC decision and its impact on the oil price.

The dollar regained the ground lost last night against the euro: the EUR/USD exchange rate has fallen back below 1.16. The prospects of a widening interest rate spread outweigh the general optimism displayed by the markets.