Prospects of below-average temperatures in the coming two weeks, a tight supply picture and soaring coal and EUA prices pushed European gas prices further high on Tuesday. The coal API 2 Cal 2022 contract moved closer to the $80/t mark, mirroring a sharp increase in Chinese coal prices on worries of sustained tightness and strong demand ahead of the summer peak demand period.

On the EU gas supply side, Russian gas imports are in the bottom part of the historical range since the beginning of May at 320 mm cm/day while LNG sendouts from NW European terminals (UK, BE, NL, Montoir and Dunkerque) dropped to 135 mm cm/day on average since 1 May compared to 186 mm cm/day on average in April 2021.

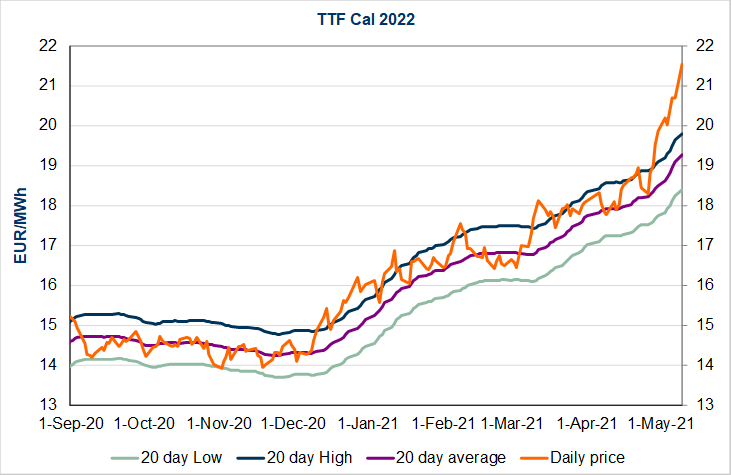

Finally, Europe gas stocks sit at only 32 Bcm on 10 May, 13 Bcm below the 5-year average for this time of year. In this context, the benchmark TTF year-ahead contract breached the €22/MWh level for the first time since late 2018.