Deceleration of activity and lower interest rates in China

China’s GDP growth declined to +4% yoy in the last quarter of 2021. This is a less sharp deceleration than expected, thanks in particular to the…

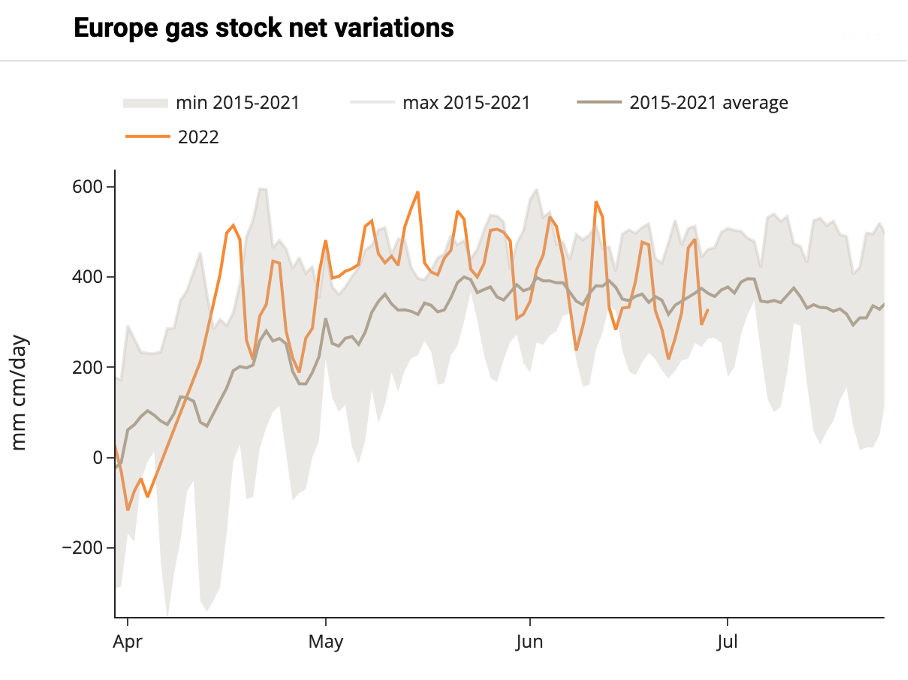

Bulls kept control of European gas prices on Wednesday with concerns over a slowdown in storage injections in June (see below chart) due to the drop in Russian gas flows through the Nordstream 1 pipeline and the shutdown of the Freeport LNG terminal providing strong support. Europe gas stock fullness rate sits at 57.8% as of June 28, in line with the 2015-2021 average level for this time of year. News that loadings from Shell’s Prelude FLNG terminal in Australia may be disrupted for two weeks due to work bans by unions asking for higher salaries and that Russia was not in diplomatic contact with Canada and Germany over the Nordstream 1 turbine issue may have also played into the bullish sentiment.

TTF front-month prices traded above the €140/MWh for the first time since March 11 yesterday while TTF WIN 22 prices widened their premium to WIN 23 prices above the €50/MWh mark. Finally, TTF ICE Cal 2023 prices settled above the €100/MWh mark for the first time ever as well.

No major move in terms of fundamentals at the opening today with Norwegian gas export capacity still constrained by 29 mm cm/day today but due to increase from tomorrow. Rising wind speeds in Germany could also weigh on spot gas prices. The progressive return from maintenance of French LNG import terminals this week could also provide some relief to the European gas balance in the short term. Nevertheless, the upcoming shutdown of the Nordstream 1 pipeline for annual maintenance from July 11 remains a key supply event with some market players concerned about the resumption of flows once the outage will end. From a technical point of view, TTF front-month prices still have some upside in the short-term even they are trading in overbought territory for a few weeks now, which should keep volatility at a high level.