Profit taking drove EUAs back in middle of the trading range

The European power spot prices are mixed for today compared to Friday as the dropping nuclear availability and higher clean gas costs supported the French…

European gas prices were very volatile yesterday, torn between the continuation of Russian gas exports (which averaged 247 mm cm/day yesterday, compared to 248 mm cm/day on Friday) and the tightening of sanctions (including the blocking of certain Russian banks’ access to the SWIFT international payment system) which suggests that at some point these exports could be disturbed.

At the close, NBP ICE March 2022 prices increased by 12.230 p/th day-on-day (+5.42%), to 237.780 p/th. TTF ICE March 2022 prices were up by €4.17 (+4.42%), closing at €98.595/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 34 euro cents (-0.55%), closing at €61.353/MWh.

In Asia, JKM spot prices increased by 12.12%, to €112.751/MWh; April 2022 prices increased by 2.03%, to €85.007/MWh.

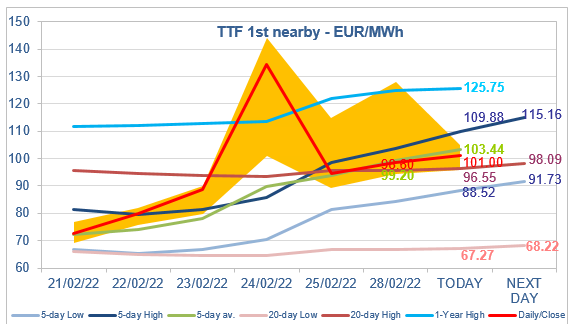

The resistance of the 1-Year High target worked quite well yesterday, and TTF ICE April 2022 prices finally closed much below, around the 5-day average. They are increasing this morning, but moderately. The market seems to assume that, as long as Russian supply continues to flow, there is no need to push prices much higher (ie back to the 1-Year High). But, given the levels of Asia JKM spot prices and the price of the most expensive gasoil switching possibilities (estimated around €114/MWh), any price drop should be limited. Therefore, in the absence of decisive fundamental information, prices could trade today in the zone between the 20-day High and the 5-day High.