DUCs at rock bottom

Japanese refining scaled back in the first weeks of January to 2.86 mb/d while we expected runs to remain at 2.95 mb/d. Crude inventories rose by 3…

European gas prices were almost stable on the spot and the two front months yesterday as ongoing strong LNG sendouts and profit taking continued to dampen the bullish pressure; the sharp drop in Norwegian flows (to 316 mm cm/day on average yesterday, compared to 341 mm cm/day on Wednesday, due to an unplanned outage at the giant Troll gas field) lent moderate support. By contrast, prices on the rest of the curve continued to post stronger gains, reducing the backwardation. Indeed, amid strong concerns on Russia-Ukraine tensions, Asia JKM prices (+7.30% on the spot yesterday, to €90.331/MWh; -1.30% for the March 2022 contract, to €77.396/MWh; +1.62% for the April 2022 contract, to €88.221/MWh) continued to send bullish signals for next summer.

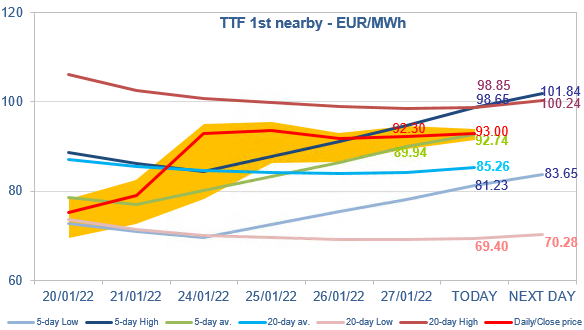

At the close, NBP ICE February 2022 prices increased by 0.790 p/th day-on-day (+0.36%), to 219.960 p/th. TTF ICE February 2022 prices were up by 46 euro cents (+0.51%), closing at €92.301/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €1.89 (+3.64%), closing at €53.754/MWh.

Yesterday, TTF ICE February 2022 prices continued to trade almost perfectly between the 5-day average and the 5-day High. The 5-day High for today seems too high and more difficult to reach, unless Asian buyers increase their bids more aggressively. Therefore, prices could stabilize around the 5-day average today. In case of a significant fundamental (or political) news, they could rise towards the 5-day High or drop towards the 20-day average.