Quarterly options’ expiry triggered another sell-off in the carbon market

The European power spot remained once again at the same level yesterday as forecasts of stronger solar generation and weaker demand offset the higher gas…

European spot gas prices increased yesterday, supported by higher demand. The trend was more mixed for curve prices which adopt a wait-and-see position in a context of stable Russian flows (at 104 mm cm/day on average). On their side, Norwegian flows increased very slightly to 322 mm cm/day on average yesterday, compared to 320 mm cm/day on Monday.

The drop in coal prices (-1.83% for API2 1st nearby prices, -2.51% for Cal 2023 prices) exerted some downward pressure.

At the close, NBP ICE July 2022 prices dropped by 5.160 p/th (-3.00%), to 166.750 p/th, equivalent to €65.930/MWh. TTF ICE July 2022 prices were down by 28 euro cents (-0.22%), closing at €129.176/MWh. On the far curve, TTF ICE Cal 2023 prices increased by 50 euro cents (+0.51%), closing at €97.807/MWh.

In Asia, JKM spot prices dropped by 2.00%, to €117.722/MWh; August 2022 prices dropped by 0.24%, to €120.032/MWh.

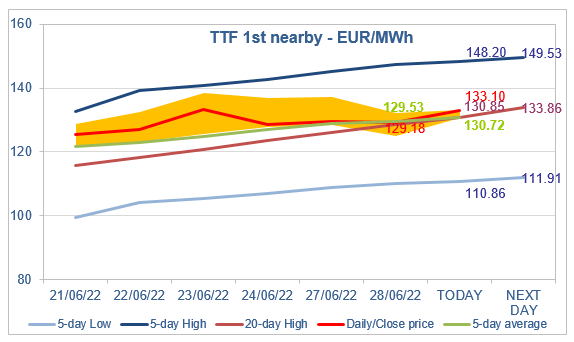

Despite some attempts, TTF 1st nearby prices did not manage to really break the support of the 5-day average, closing very slightly below this level. They are rebounding this morning. Among market participants, growing concerns on the weakening of storage injections in the past days seem to prevent prices from falling below the 20-day High (€130.85/MWh for today) and accelerating their “normalization” process. Moreover, Nord Stream 1 gas flows will be completely cut-off on 11-21 July for planned annual maintenance. In the absence of a decisive fundamental element, prices could continue to trade around the 5-day average (and the 20-day High).