Mobility takes a toll

Brent prompt futures remained at 54.7 $/b on early Thursday. Mobility across Europe and the US is reportedly lower in early January as most countries…

European gas prices rebounded slightly yesterday, supported by the additional drop in pipeline supply. Indeed, Russian flows weakened again yesterday, to 211 mm cm/day on average, compared to 229 mm cm/day on Wednesday. Norwegian flows dropped to 315 mm cm/day on average, compared to 319 mm cm/day on Wednesday. But as these declines are not due to supply issues but rather to buyers’ arbitrages, the price impact was limited.

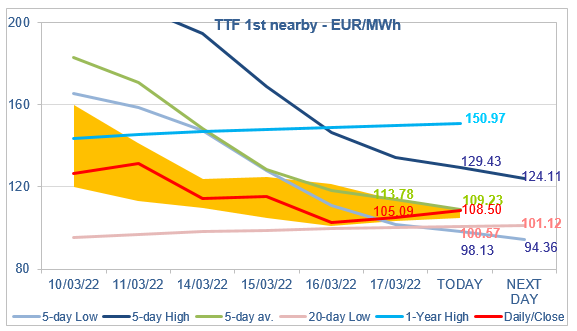

At the close, NBP ICE April 2022 prices increased by 8.970 p/th day-on-day (+3.72%), to 249.780 p/th. TTF ICE April 2022 prices were up by €2.46 (+2.40%), closing at €105.088/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €2.06 (+3.41%), closing at €62.596/MWh.

In Asia, JKM spot prices dropped by 0.31%, to €110.447/MWh; May 2022 prices increased by 5.16%, to €109.405/MWh.

Paradoxically, the current drop in Russian flows sends a rather bearish signal. It suggests that contract buyers are not in a panic, probably reassured by improving stock levels and the prospect of a high Norwegian supply this summer. But the other main components of supply cannot be taken for granted. There is a lingering risk on Russian supply, and now that European prices tend to drop below Asia JKM prices a drop in LNG supply to Europe cannot be excluded. If headwinds were to hit these two supply components, contract buyers would rush to the spot… where they would meet with structural spot buyers. The impact on prices is then easy to imagine. For the moment, TTF ICE April 2022 prices are finding support around the 20-day Low and resistance around the 5-day average. An “equilibrium” zone between the bullish zone around the 1-Year High (€150.97/MWh for today) and the bearish zone around the maximum coal switching level (€81/MWh for today)! But this “equilibrium” will certainly not last and at some point the market will have to choose.