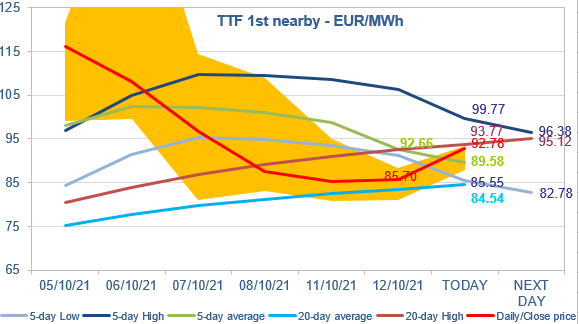

EUAs recouped recent gains on renewed gas supply concerns

Despite higher gas prices and decreasing temperatures, most European power spot prices faded yesterday on forecasts of surging wind production. The day-ahead prices averaged 254.32€/MWh…