Longer-dated refining margins rallying ahead of the winter

Crude oil prices climbed higher to 74 $/b for ICE Brent front-month contract ahead of the Nicolas weather event, reclassified as a hurricane in the last…

Amid unchanged fundamentals, European gas prices weakened slightly overall yesterday. The (moderate) drop in Asia JKM prices (-1.91%, to €107.482/MWh, on the spot) helped accompany the drop. On the spot pipeline supply side, Norwegian flows were slightly up yesterday, at 348 mm cm/day on average, compared to 343 mm cm/day on Wednesday. Russian supply was slightly down, to 283 mm cm/day on average, compared to 285 mm cm/day on Wednesday.

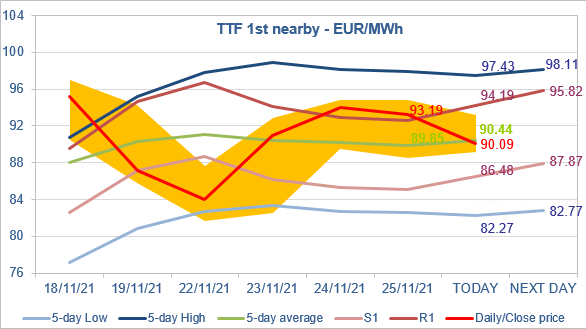

At the close, NBP ICE December 2021 prices dropped by 1.710 p/th day-on-day (-0.73%), to 233.660 p/th. TTF ICE December 2021 prices were down by 79 euro cents (-0.84%) at the close, to €93.194/MWh. On the far curve, TTF Cal 2022 prices were up by 39 euro cents (+0.69%), closing at €56.547/MWh, with the spread against the coal parity price (€39.848/MWh, -0.80%) widening.

Intraday volatility was low again yesterday, with TTF ICE December 2021 prices seeming to have found an equilibrium around the 5-day average (with a slight upward bias). The support and resistance levels S1 and R1 are now the most relevant the set the likely trading range in this low volatility environment. But, as yesterday, the bias remains upward given the spread with JKM prices.