Neutral carbon and easing power prices

The NWE power spot prices observed mixed variations yesterday, the French prices strongly correcting downward from its peak amid forecasts of lower demand and improved…

European gas prices eased slightly yesterday as the bullish momentum fueled by President Putin’s announcement that Russia will seek payment in rubles for gas sold to “unfriendly” countries faded a little. The general sentiment was that, under contractual arrangements, the supplier cannot unilaterally change the payment currency. The increase in pipeline flows also exerted downward pressure. Indeed, Norwegian flows rebounded strongly yesterday to 322 mm cm/day on average, compared to 308 mm cm/day on Wednesday, as the unplanned outage on the giant Troll field was fixed. Russian flows were also up, averaging 236 mm cm/day, compared to 231 mm cm/day on Wednesday.

At the close, NBP ICE April 2022 prices dropped by 12.680 p/th day-on-day (-4.57%), to 264.820 p/th. TTF ICE April 2022 prices were down by €5.39 (-4.61%), closing at €111.608/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 24 euro cents (-0.34%), closing at €71.395/MWh.

In Asia, JKM spot prices increased by 13.10%, to €119.856/MWh; May 2022 prices increased by 1.72%, to €107.615/MWh.

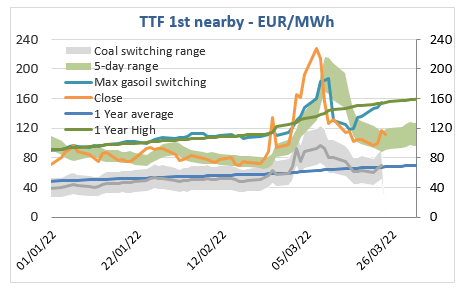

For those who attended our webinar yesterday, the chart above is one of those we showed, with a shorter observation period and the addition of the 5-day range (set by the 5-day Low and the 5-day High targets). In addition to the bearish fundamentals we mentioned above, we believe profit taking has also contributed to pull prices down yesterday. Prices are weakening again this morning, trading close to the 5-day average (€106.23/MWh). If this support is broken, the 20-day Low (€99.97/MWh for today) will oppose a stronger support. But prices can still drop towards the 5-day Low (€91.51/MWh for today). As this level is above the coal switching range (whose maximum is currently around €89/MWh), such a decline is sustainable because it would not break the fundamental equilibrium.