Roller coaster

Financial markets continue to move in tandem with news from the Russian-Ukrainian border. At the end of last week, there was widespread pessimism ahead of…

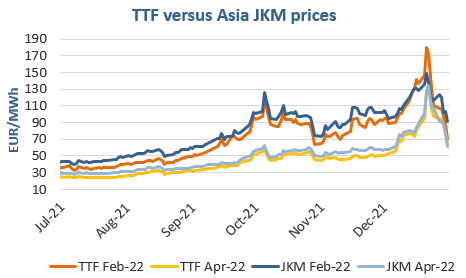

European gas prices dropped significantly end December, pressured by lower heating demand (as temperatures rose significantly above normal) and higher LNG supply. Indeed, the moderation in Asia LNG imports (China LNG imports even dropped by 1.4% y-o-y in December) led to a strong increase in LNG flows to Europe in December: +19% m-o-m and +42% y-o-y. On the spot pipeline supply side, Norwegian flows remained close to their maximum, averaging 342 mm cm/day during the last week of December. Russian supply was lower, averaging 244 mm cm/day, compared to 264 mm cm/day the week before.

At the close on Friday, NBP ICE February 2022 prices dropped to 170.640 p/th (-36.29% week-on-week). TTF ICE February 2022 prices dropped to €70.343/MWh (-36.32% w-o-w). On the far curve, TTF Cal 2022 prices expired at €79.064/MWh on December 30 (-29.60% w-o-w). TTF Cal 2023 prices closed on Friday at €41.330/MWh (-17.88% w-o-w).

Russian supply dropped further since the start of the year. Moreover, Indonesia, the world’s biggest exporter of thermal coal banned last Saturday coal shipments because of concerns it could not meet its own power demand; this could increase LNG needs from China, India, Japan, and South Korea, which together received 73% of Indonesian coal exports in 2021. Therefore, after the sharp drop of end December, European gas prices could rebound today, particularly as they are technically oversold. However, lower liquidity (the UK market is closed today) could limit price movements.