EUAs rose above 52€/t on strong bullish momentum and spiking gas prices

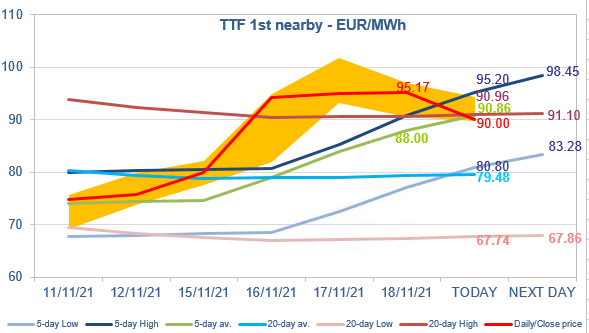

As expected, the European power spot prices rose further up yesterday amid forecasts of falling temperatures and renewable generation. The day-ahead prices in Germany, France,…