Prices maintained their strong uptrend

European gas prices maintained their strong uptrend yesterday, still supported by tight domestic fundamentals, while competition with Asia for LNG supply does not show yet…

European gas prices increased yesterday, supported by lower Norwegian flows (down to 313 mm cm/day on average, compared to 346 mm cm/day on Tuesday, due to planned maintenance at the giant Troll gas field and the Kollsnes processing plant) and higher coal prices (+1.29% for API2 1st nearby prices, +4.40% for Cal 2023 prices). On their side, Russian flows were very slightly up, averaging 207 mm cm/day, compared to 205 mm cm/day on Tuesday.

At the close, NBP ICE May 2022 prices increased by 4.550 p/th day-on-day (+2.63%), to 177.880 p/th. TTF ICE May 2022 prices were up by 46 euro cents (+0.49%), closing at €94.231/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €2.43 (+3.11%), closing at €80.519/MWh.

In Asia, JKM spot prices increased by 1.70%, to €79.145/MWh; June 2022 prices dropped by 0.27%, to €79.250/MWh.

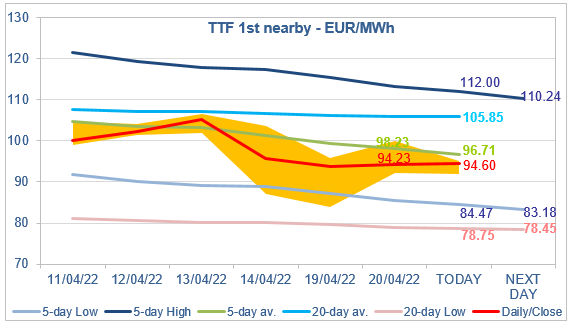

The increase in coal prices drove the maximum coal switching level up yesterday, to €102/MWh (compared to €99/MWh on Tuesday), which offered upside potential to TTF ICE May 2022 prices. But the latter failed to break the resistance of the 5-day average, thus maintaining their slight bearish bias. Prices seem to have found an equilibrium around the middle of the range set by the 5-day Low (€84.47/MWh for today) and the 5-day High (€112.00/MWh for today). The improvement in spot fundamentals prevents them from rising towards the latter, and the potential increase in gas-fired power generation (at the expense of coal) prevents them from dropping/remaining towards/at the former.