SPR release in the void ?

Crude prices remained pressured, sticking to the 80-82 $/b range, as the possibility of a US SPR release limited prompt tightness. With such growing political…

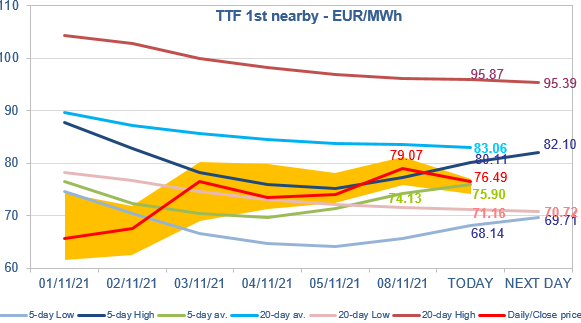

European gas prices increased yesterday as the hopes of an increase in Russian flows have been dashed. Indeed, Gazprom did not book extra transportation capacity at daily auctions on Sunday, and actually Russian flows remained almost stable yesterday, at 252 mm cm/day. On their side, Norwegian flows were up, averaging 347 mm cm/day, compared to 338 mm cm/day on Friday. The rise in Asia JKM prices (+4.80%, to €92.997/MWh, on the spot; +1.48%, to €94.669/MWh, for the December 2021 contract) and in parity prices with coal for power generation (both coal and EUA prices were up) also provided support to prices.

At the close, NBP ICE December 2021 prices increased by 11.470 p/th day-on-day (+5.99%), to 202.900 p/th. TTF ICE December 2021 prices were up by €5.05 (+6.82%) at the close, to €79.074/MWh. On the far curve, TTF Cal 2022 prices were up by €2.37 (+4.95%), closing at €50.162/MWh, and the spread against the coal parity price (€33.745/MWh, +4.98%) increased.

Contrary to what we might have expected, the market was not so bullish yesterday, with TTF ICE December 2021 prices closing between the 5-day High and the 20-day average. And this morning, they are weakening. It seems the market has decided to adopt a wait-and-see position, i.e. a gradual “normalization” by moving the 5-day range smoothly inside the 20-day range. By the end of the week (depending in particular on the evolution of Russian flows), it will still be time to make the choice of an uptrend or not (the 5-day average rising above the 20-day average or not).