Strong downward correction in Europe

European gas prices dropped significantly yesterday, pressured by more comfortable pipeline supply and profit taking after the previous sessions’ strong gains. Russian flows were stable…

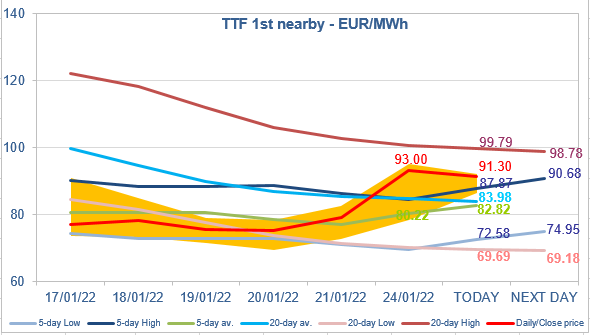

European gas prices increased strongly yesterday as a risk premium on the Russia-Ukraine conflict is building. Even the statements of Russian government spokesman saying that Russia has been a reliable energy supplier to Europe even at difficult times in relations did not seem to reassure the market. The rise in Asia JKM prices (+14.72% on the spot, to €72.163/MWh; +14.20% for the March 2022 contract, to €75.909/MWh) helped accompany the bullish momentum as it shows that Asian buyers are not ready to give up all available LNG cargos to their European counterparts. On the pipeline supply side, Norwegian flows continued their rebound, reaching 346 mm cm/day yesterday, compared to 342 mm cm/day on Friday. Russian supply was also up, averaging 198 mm cm/day, compared to 190 mm cm/day on Friday.

At the close, NBP ICE February 2022 prices increased by 35.430 p/th day-on-day (+18.72%), to 224.740 p/th. TTF ICE February 2022 prices were up by €14.02 (+17.75%), closing at €93.000/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €3.90 (+8.73%), closing at €48.633/MWh.

TTF ICE February 2022 prices broke yesterday the resistance of the 20-day average and the 5-day High. They are weakening this morning, probably because of profit taking by financial participants. But, fueled by geopolitical tensions over Ukraine, the short-term trend seems bullish now, with the 20-day average and the 5-day average becoming support levels.