EUAs reversed in the afternoon after climbing to a fresh record

The power spot prices eroded 9.17€/MWh to reach 55.15€/MWh on average in Germany, France, Belgium and the Netherlands, pressured by forecasts of stronger renewable production.…

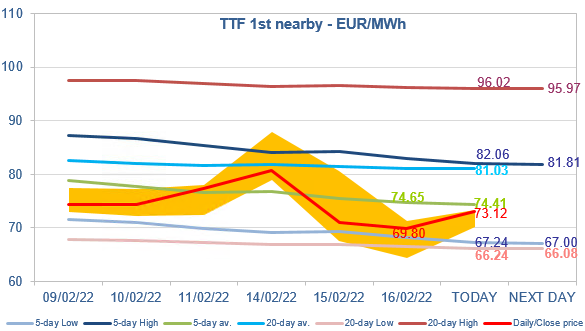

European gas prices were mixed yesterday. The apparent easing of tensions on the Ukrainian border exerted downward pressure on curve prices. By contrast, spot prices were supported by lower Russian flows (down to 187 mm cm/day on average yesterday, compared to 212 mm cm/day on Tuesday, probably because weaker spot prices led to a reduction in offtakes on long-term contracts). The trend in Asia JKM prices (-14.03% on the spot, to €65.476/MWh; +0.50% for the April 2022 contract, to €69.230/MWh) showed competition for flexible LNG cargoes is still expected to be stronger from April.

At the close, NBP ICE March 2022 prices dropped by 3.970 p/th day-on-day (-2.32%), to 166.920 p/th. TTF ICE March 2022 prices were down by €1.12 (-1.58%), closing at €69.795/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €1.46 (-2.82%), closing at €50.409/MWh.

The behavior of Russian flows suggests a limited downside potential for TTF spot and near curve prices for the time being. Yesterday, TTF ICE March 2022 prices benefited from the support of both the 5-day Low and the 20-day Low targets. They are rebounding this morning. But, given the levels of Asia JKM prices (which exempt European buyers from overbidding), the rebound could be limited.