EUAs recovered from 5-month low as compliance buyers stepped in

The European power spot prices surged near 340€/MWh yesterday, lifted by a combination of spiking gas prices, a wind shortage and a continuously weak nuclear…

European gas prices maintained their bullish trend yesterday, supported by the prospect of an additional drop in Russian flows. Indeed, Gazprom said yesterday it had halted operations at one of three operational compressor units at the Portovaya compressor station due to maintenance issues. This should remove a further 33 mm cm/day of Russian exports from today.

Yesterday, Russian supply weakened again, averaging 136 mm cm/day, compared to 143 mm cm/day on Tuesday. By contrast, Norwegian flows continued to rebound, averaging 318 mm cm/day on average, compared to 284 mm cm/day on Tuesday.

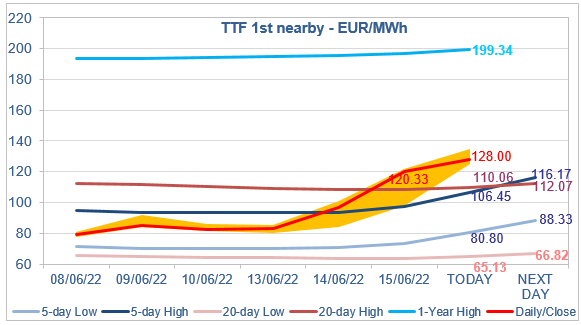

At the close, NBP ICE July 2022 prices increased by 61.230 p/th (+31.15%), to 257.78 p/th, equivalent to €102.540/MWh. TTF ICE July 2022 prices were up by €23.292 (+24.00%), closing at €120.332/MWh. On the far curve, TTF ICE Cal 2023 prices increased by €7.011 (+8.36%), closing at €90.919/MWh.

In Asia, JKM spot prices increased by 20.03%, to €94.516/MWh ; August 2022 prices increased by 22.25%, to €110.781/MWh.

With the accumulation of bullish news, TTF 1st nearby prices are now anchored well above the maximum coal switching level, currently at €100.44/MWh,… waiting for evidence of demand destruction in the power generation sector. Until that happens, only profit taking by financial players could possibly limit the upward pressure.