EUAs waned towards 60€/t as the third quarter ended

The power spot prices dropped yesterday in northwestern Europe, pressured by forecasts of strong wind and solar generation, higher French nuclear availability and slightly weaker…

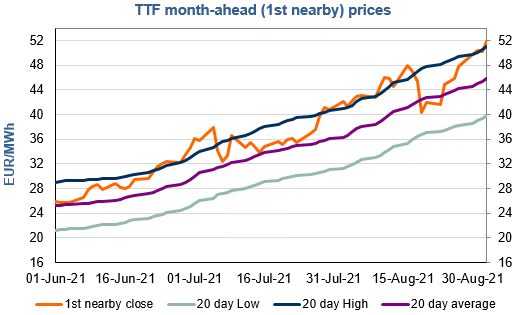

After taking a breather on Wednesday, European gas prices resumed their uptrend yesterday, still supported by tight fundamentals. Indeed, Russian supply remained weak yesterday, averaging 287 mm cm/day (compared to 288 mm cm/day on Wednesday), as both flows through Poland and Ukraine remained below their levels of last week. Norwegian flows were down, averaging 292 mm cm/day (compared to 314 mm cm/day on Wednesday), due to planned maintenance works.

The additional rise in Asia JKM prices (+2.13% for the October 2021 contract, to €53.052/MWh) and in parity prices with coal for power generation (both coal and EUA prices were up) also provided support.

At the close, NBP ICE October 2021 prices increased by 4.250 p/th day-on-day (+3.33%), to 132.00 p/th. TTF ICE October 2021 prices were up by 168 euro cents (+3.35%) at the close, to €51.916/MWh. On the far curve, TTF Cal 2022 prices were up by 94 euro cents (+2.82%), closing at €34.295/MWh, slightly above the coal parity price (€33.890/MWh).

Tight fundamentals could continue to lend support to European gas prices today. However, profit taking by financial participants and technical resistances (€52.129/MWh on TTF October 2021 and €34.437/MWh on TTF Cal 2022) could contribute to limit gains.