Bond yields and the euro rebound

We spent the week noting the curious decline in bond yields while the US figures were frankly good. If they rebounded yesterday, it was not…

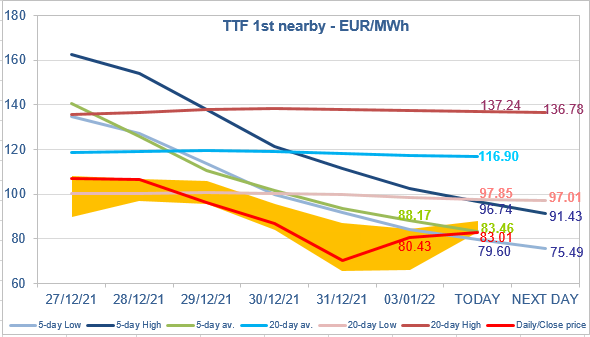

European gas prices rebounded yesterday, supported by the additional drop in Russian flows, concerns on a possible ban of Indonesia coal exports in January and technical buying. Indeed, Russian supply dropped to 183 mm cm/day on average yesterday, compared to 251 mm cm/day on Friday. Norwegian flows remained close to their maximum, averaging 352 mm cm/day yesterday, compared to 351 mm cm/day on Friday.

At the close yesterday, TTF ICE February 2022 prices were up by €10.09 (+14.35% d-o-d), closing at €80.434/MWh On the far curve, TTF ICE Cal 2023 prices were up by €3.48 (+8.42%), closing at €44.809/MWh.

Asia JKM prices sent mixed signals yesterday: -18.64% on the spot, to €70.759/MWh; +0.69% for the February 2022 contract, to €92.162/MWh. But, as these prices are both above European levels (TTF day-ahead prices were assessed at €64.400/MWh yesterday), LNG arbitrage could now favor the Asian market, leading to a reduction in LNG flows to Europe (along with mild weather, higher LNG supply was the main factor explaining the sharp decline in European gas prices end December). Therefore, we believe the downside potential for TTF February 2022 prices is currently limited and they could continue to rebound. This rebound is also backed by the technical configuration, which favors a price rise inside the 5-day range.