EUAs rebounded on slow activity induced by the public holiday

The European power spot prices unsurprisingly rebounded yesterday as a consequence of the power demand returning to normal levels with the holiday now passed, although…

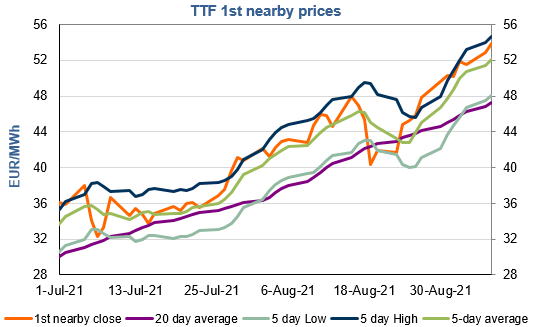

European gas prices extended gains yesterday. Russian supply rebounded, averaging 287 mm cm/day (compared to 278 mm cm/day on Monday), thanks mainly to the increase in flows through Poland to the Mallnow interconnection point, but they remained well below the levels of end August (313 mm cm/day). Norwegian flows were stable, at 282 mm cm/day on average, but they are expected to drop today due to planned maintenance at Troll. The market seems to have been more sensitive to this expected drop in Norwegian flows than to the rebound in Russian flows. The rise in Asia JKM prices (+1.59% for the October 2021 contract, to €53.853/MWh) and in parity prices with coal for power generation provided additional support.

At the close, NBP ICE October 2021 prices increased by 2.330 p/th day-on-day (+1.74%), to 136.440 p/th. TTF ICE October 2021 prices were up by 103 euro cents (+1.96%) at the close, to €53.908/MWh. On the far curve, TTF Cal 2022 prices were up by 45 euro cents (+1.29%), closing at €35.541/MWh, slightly increasing the spread with the coal parity price (€34.779/MWh).

As expected, Norwegian flows are down this morning (to 261 mm cm/day). European gas balances should therefore remain tight, with prices likely to continue to increase. However, technical resistances (the first at €54.202/MWh on TTF October 2021 and €35.536/MWh on TTF Cal 2022) could contribute to limit gains.