Outright crude crashes

By falling below 80 $/b, ICE Brent front-month future declined by close to 4.5% within a day. Yet, front-month time spreads remained supported, at 127…

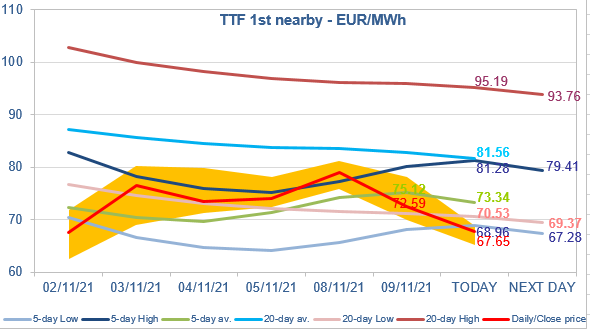

European gas prices dropped yesterday as the long-awaited rise in Russian flows seems to materialize. Indeed, Gazprom said yesterday it had started to implement a plan for gas injection this month into five of its European storage facilities. Yesterday, Russian supply was higher (to 269 mm cm/day on average, compared to 252 mm cm/day on Monday), meaning Gazprom made more intensive use of its existing capacity. And as it booked yesterday 10 mm cm/day of additional day-ahead capacity at Velke Kapusany for today delivery, flows are expected to continue to rise. On their side, Norwegian flows were slightly lower, averaging 340 mm cm/day, compared to 347 mm cm/day on Monday. The drop in Asia JKM prices (-4.87%, to €88.470/MWh, on the spot; -1.24%, to €93.495/MWh, for the December 2021 contract) and in parity prices with coal for power generation (both coal and EUA prices were down) helped accompany the bearish momentum.

At the close, NBP ICE December 2021 prices dropped by 15.720 p/th day-on-day (-7.75%), to 187.180 p/th. TTF ICE December 2021 prices were down by €6.49 (-8.20%) at the close, to €72.587/MWh. On the far curve, TTF Cal 2022 prices were down by €3.47 (-6.92%), closing at €46.693/MWh, and the spread against the coal parity price (€32.751/MWh, -2.94%) narrowed.

TTF ICE December 2021 prices managed to close yesterday above their 5-day Low and 20-day Low supports. But the pressure of the increase in Russian flows is such that they are breaking these supports this morning. However, we should keep in mind that the European gas market equilibrium remains fragile given the relatively low stock levels and the higher levels of Asia JKM prices. Therefore, at such technically oversold levels, a rebound cannot be excluded.