Gas & Power Report: Gas prices continue to ease in Europe

Gas & Power Podcast #43 In this weekly podcast for Gas & Power, we discuss about the continuation of the bearish trend in European gas…

European gas prices weakened yesterday. Russian flows increased again, averaging 227 mm cm/day, compared to 218 mm cm/day on Wednesday. Norwegian flows were also up, rebounding to 320 mm cm/day on average, compared to 312 mm cm/day on Wednesday. Comments from Russia Deputy Prime Minister Alexander Novak saying yesterday that around half of the 54 companies that have contracts with Gazprom Export have already opened accounts with Gazprombank in order to comply with Moscow’s new ruble-based payment system also contributed to exert downward pressure.

However, the rise in coal prices (+0.25% for API2 1st nearby prices, +2.86% for Cal 2023 prices) lent some support, particularly to far curve prices.

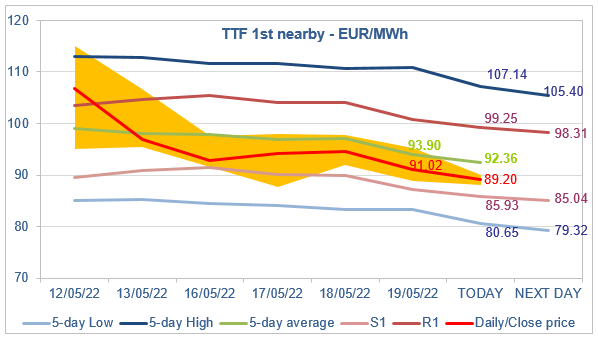

At the close, NBP ICE June 2022 prices dropped by 13.240 p/th (-7.28%), to 168.740 p/th, equivalent to €67.882/MWh. TTF ICE June 2022 prices were down by €3.51 (-3.72%), closing at €91.024/MWh. On the far curve, TTF ICE Cal 2023 prices dropped by 93 euro cents (-1.20%), closing at €76.513/MWh.

In Asia, JKM spot prices increased by 1.76%, to €73.525/MWh; July 2022 prices increased by 1.79%, to €70.235/MWh.

Thanks to lower EUA prices, the month-ahead coal switching levels dropped yesterday: to €102.42/MWh for the maximum and to €78.39/MWh for the average. Adding to alleviating concerns over Russian gas payment in rubles, this maintained TTF ICE June 2022 prices below their 5-day average. They seem on track to drop to the S1 support level soon. For the 5-day Low, one will have to wait a little longer, hoping that no major fundamental element stops the downward momentum.