Optimism returns to the markets but rates continue to rise

The temporary deal on the US debt ceiling also gives the Democrats time to agree on the stimulus packages that the Biden administration wants to push through.…

European gas prices dropped again on Friday, pressured by still-comfortable spot fundamentals, as storages show (they switched to net injection mode since 22 March). In particular, Russian flows were up on Friday, averaging 245 mm cm/day, compared to 236 mm cm/day on Thursday. Norwegian flows were almost stable, averaging 323 mm cm/day, compared to 322 mm cm/day on Thursday.

On the political side, the US and the EU announced on Friday the creation of a joint Task Force to reduce Europe’s dependence on Russian fossil fuels and to set out the parameters of new EU-US cooperation (see our news).

Moreover, EU leaders agreed to work together on collective gas procurement, “instead of outbidding each other and driving prices up”. In terms of market intervention and market design for gas and electricity, the European Commission will bring concrete proposals in May.

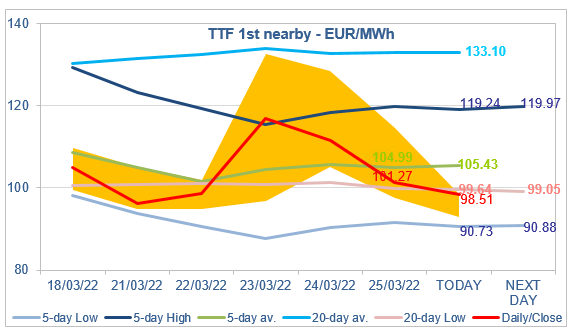

At the close, NBP ICE April 2022 prices dropped by 28.210 p/th day-on-day (-10.65%), to 236.610 p/th. TTF ICE April 2022 prices were down by €10.34 (-9.26%), closing at €101.269/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €3.13 (-4.38%), closing at €68.266/MWh.

In Asia, JKM spot prices dropped by 13.80%, to €103.319/MWh; May 2022 prices dropped by 0.59%, to €106.985/MWh.

TTF ICE April 2022 prices closed slightly above the 20-day Low support on Friday. But, with the combined pressure of bearish spot fundamentals and to a lesser extent Friday’s political announcements, this support is being broken this morning. A drop towards the 5-day Low (€90.73/MWh for today) cannot be ruled out. As this level is above the coal switching range (whose maximum is currently around €87/MWh, down on Friday), such a decline is sustainable because it would not break the fundamental equilibrium.